Pakistan eyes investment from Saudi, China as Mineral Summit begins in Islamabad from today.

Pakistan is set to host a two-day minerals summit in Islamabad starting Tuesday, bringing together ministers and executives from major mining companies across Saudi Arabia, China, the U.S., and other nations. The event aims to attract global investment into the country’s estimated $6 trillion worth of untapped mineral resources.

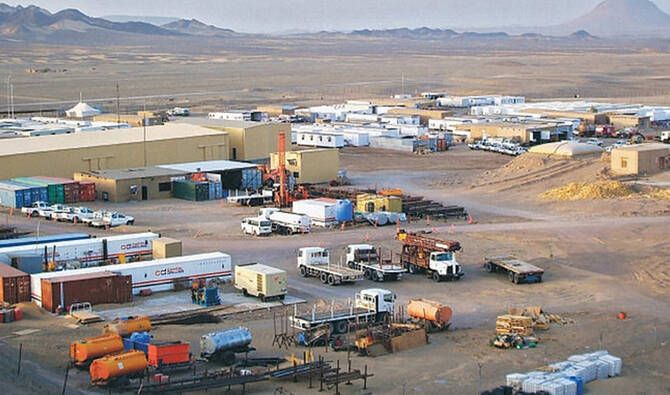

Amid an ongoing economic crisis, Pakistan views its mineral wealth as a key to economic revival. The country possesses vast deposits of copper and gold, notably the Reko Diq site in Balochistan, which holds about 5.9 billion tons of ore. Barrick Gold, which owns half of the project, regards it as one of the most significant undeveloped copper-gold resources globally, with potential to boost Pakistan’s struggling economy.

The summit is being organized by the Oil and Gas Development Company Limited (OGDCL) in coordination with the government and international partners. According to Petroleum Minister Ali Pervaiz Malik, the Pakistan Minerals Investment Forum, scheduled for April 8–9, is expected to draw around 2,000 participants, including high-ranking foreign delegates.

Speaking to the media on Monday, Malik stated that both government officials and private sector leaders from mining industries are set to attend. Countries such as Turkiye will be part of the discussions along with others.

He also confirmed high-level participation from China, Saudi Arabia, Azerbaijan, and the United States, highlighting the global interest in Pakistan’s mineral potential.

During the summit, Pakistan will officially introduce its National Minerals Harmonization Framework 2025, a newly developed, investor-friendly policy designed to draw foreign investment into the mineral sector.

The forum will also include the signing of major agreements and MoUs between Pakistan and other participating countries. Malik emphasized that the government intends to move beyond declarations by formalizing and executing actual agreements that lead to practical implementation.

With mining identified as a key sector for economic growth, Pakistan hopes to reduce import dependency and boost exports by leveraging international partnerships and capital. This strategy is seen as crucial for stabilizing the country’s $350 billion economy, which has been under pressure in recent years.

To counteract its financial difficulties, Pakistan has intensified trade and investment outreach to neighboring and regional countries, including those in Central Asia and the Gulf, aiming to bolster its reserves and ease pressure on its currency and balance of payments.

In 2023, the country established the Special Investment Facilitation Council (SIFC), a civil-military initiative, to fast-track foreign investment into priority sectors, particularly mining and minerals, as part of broader economic recovery efforts.

Related Posts

{kind=link}